Catastrophic risks are bad news for your insurance

There is no good news in the IPCC’s AR6 pt II report on impacts of ongoing global warming. If frequent, catastrophic risks will be uninsurable.

The problem with most extreme weather events like wildfire, floods, droughts, cyclones, etc., is that their catastrophic effects normally cover large areas.

Insurance companies are only profitable if premium payments produce more income than is paid out on claims for losses over the number of customers. If only a small proportion of insured people make claims, the company can still profitably sell the policies for a small fraction of the average payout, such that people can expect full payouts on the claims made, even though the premium paid is only a fraction of the payout.

Even in the case of widespread catastrophes, if such catastrophes are rare enough over the world, a retail insurance company can insure themselves against a huge payoff by buying re-insurance from a specialist company betting that the total number of catastrophic risk events will be small relative to the policies they sell. Both the retail insurer and the reinsurer can still make a profit to stay in business.

However, if catastrophic loss events become too common, to stay profitable insurers have to charge premium fees that become such a large fraction of the cost of the possible loss that customers simply can no longer afford to pay the premium cost, as many people and businesses located in areas such as flood planes, bush lots in fire prone regions, and low-lying coastal area susceptible to cyclones and rising sea-levels deemed to be at high risk of catastrophic losses.

Thanks to rising rates and ferocities of wildfires and intense flooding many people are discovering that their catastrophic risks of total loss in such events are no longer insurable at an affordable cost — even assuming they can find someone willing to sell them such a policy.

As explored in the attached news items, the just released IPCC report tells the insurance industry that the frequency of catastrophic risk events is likely to continue rising, at an accelerating rate as the world continues to warm. This will undoubtedly mean that many more people and businesses will no longer be able to find insurance against total loss in the event of a climate catastrophe.

The likelihood of East Coast flooding and its costs

by Antonia Settle, 03/03/2022 in The Conversation

After the floods comes underinsurance: we need a better plan: The floods affecting Australia’s eastern seaboard are a “1 in 1,000-year event”, according to New South Wales Premier Dominic Perrottet. But that’s not what science, or the insurance industry, suggests…

by K.I. Booth, 27/02/2022 in The Conversation

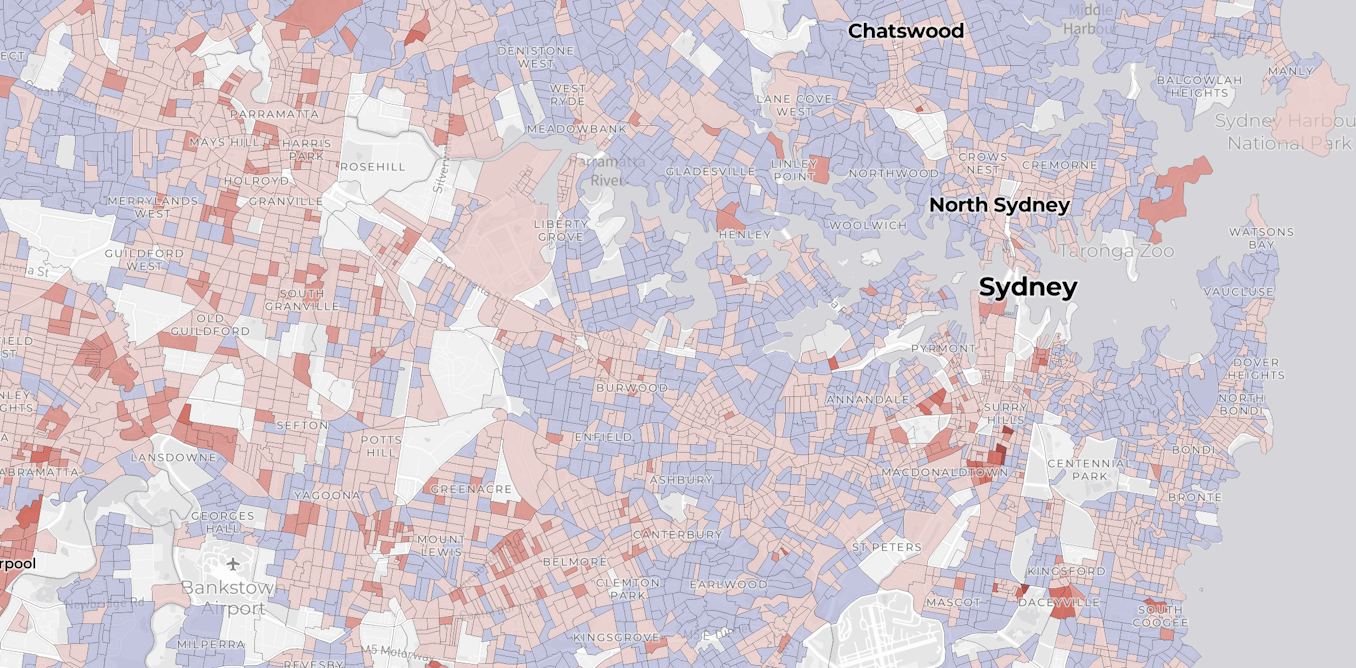

Is your neighbourhood underinsured? Search our map to find out:

Underinsurance is more common than many realise. And if you live in an area where most people don’t have enough home and/or contents insurance, the financial and social catastrophe that follows a disaster can be community-wide. Even if you’re well covered, your neighbourhood may struggle long after the dust has settled, as houses lie derelict, people struggle to bounce back and social cohesion frays….

by A. King, et al., 02/03/2022 in The Conversation

‘One of the most extreme disasters in colonial Australian history’: climate scientists on the floods and our future risk: …So how does this compare to Australia’s previous floods, such as in 2011? And can we expect more frequent floods at this scale under climate change?…

by K Reid & A King, 27/02/2022 in The Conversation

Like rivers in the sky: the weather system bringing floods to Queensland will become more likely under climate change: …We research a weather system called “atmospheric rivers”, which is causing this inundation. Indeed, atmospheric rivers triggered many of the world’s floods in 2021, including the devastating floods across eastern Australia in March which killed two people and saw 24,000 evacuate….

by K.I. Booth et al, 04/03/2022 in The Conversation

Underinsurance is entrenching poverty as the vulnerable are hit hardest by disasters: More than 70 homes were destroyed by bushfires in Western Australia this week, leaving those affected facing enormous costs. After disasters like these, insurance is not always there as needed — or as expected….

by C. Tondorf, 06/03/2022 in The Guardian

‘Worse than 2017’: Lismore faces mammoth rebuild after flood as community inundated by loss: …“How can anything upset me after this?” laughs Ken Matheson, a Lismore resident aged 65 years who lost all his possessions on Sunday night.

…Even though his house has never before had water through it, he couldn’t get flood insurance, explaining “no one will do it, no one would give it to me”.

“Hardened by a history of floods, residents are ‘getting on’ with the clean-up while waiting for politicians to address climate change” Guardian

In Australia, the political context and implications are also crystal clear. For years our LNP COALition Government has been owned and controlled by mindlessly greedy fossil fuel special interests. Both work to deny the science that shows us the world is warming at an accelerating rate from the continued burning of fossil carbon and to fill the thought space with endlessly distracting humbug and blather. The COALition’s priorities are clear in their lack of interest in using any of their Emergency Response Funds for mitigation or recovery. Burning coal clearly comes first!

As I have noted many times previously in my Climate Sentinel posts, even a child can still draw reasonable conclusions from the kinds of facts that the IPCC has exhaustively documented. Too bad for us all that the COALition are blinded to the reality of what they are doing.

In other words, wake up! smell the smoke! see the grimly frightful reality, and fight the fire that is burning up our only planet so we can give our offspring a hopeful future. This is the only issue that matters. Even the IPCC’s hyperconservative Report that looks at climate change’s global and regional impacts on ecosystems, biodiversity, and human communities makes it clear we are headed for climate catastrophe if we don’t stop the warming process.

We’ll be having a Federal Election in a couple of months. Now is our chance to rid ourselves of the dead hands of this puppet government and replace the puppets with sensible people who have committed themselves to prioritizing action on the climate emergency on the top of their agendas if elected to Parliament. Our Traffic Light Voting System can help you use our preferential voting system to its best advantage towards meeting this goal.